Key Takeaways

- SAG forecasts global AI smart glasses shipments will reach 20 million units in 2026, growing approximately 140% YoY.

- Meta will remain the clear market leader with 71% global volume share, exceeding 14 million units shipped in 2026.

- Meta launched three new AI smart glasses models under its own brand portfolio, priced between US$299 and US$399, marking the beginning of its most aggressive AI smart glasses expansion to date.

- SAG views today’s launch as the first wave of Meta’s 2026 AI smart glasses strategy, with three additional product waves expected in the coming months, including Luna, Mojito VIP, and RBM 2 Refresh.

- The launch of Starfire Kylie Edition signals Meta’s shift from positioning AI smart glasses as technology gadgets toward fashion, beauty, and lifestyle products designed to appeal to a broader consumer audience.

- Unlike smartphones, AI smart glasses are highly personal and visible products worn directly on the face. Fashion, style, comfort, brand image, and lifestyle positioning are becoming as important as hardware specifications and AI capabilities in driving adoption.

- SAG believes Qualcomm’s Snapdragon Start platform will become a major catalyst for the next phase of AI smart glasses adoption by significantly lowering development costs, reducing time-to-market, and lowering technical barriers for device makers. As hardware becomes increasingly standardized, competitive differentiation will shift toward branding, distribution channels, ecosystem integration, software experiences, and consumer trust.

- SAG believes Meta’s aggressive expansion reflects its effort to monetize AI investments, strengthen ecosystem leadership, and establish scale advantages before Apple, Google, and Samsung intensify competition.

Meta’s Biggest AI Smart Glasses Push Has Officially Begun

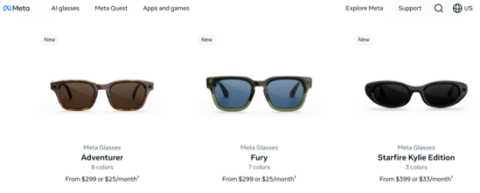

Meta today unveiled three new AI smart glasses models under its own brand portfolio, marking the company’s most aggressive consumer AI hardware expansion to date.

The newly announced Adventurer, Fury, and Starfire Kylie Edition models carry Meta branding rather than the Ray-Ban name and are priced between US$299 and US$399.

Exhibit 1: Meta Own Branded AI Smart Glasses (Adventurer, Fury, Starfire Kylie Edition) and Price

While the hardware specifications remain largely similar to the existing Meta Ray-Ban Generation 2 platform, the lower entry price improves accessibility and positions Meta to accelerate market adoption.

SAG believes this launch represents the first wave of Meta’s AI smart glasses strategy for 2026 and signals a much broader product expansion that will unfold over the next six months.

Four Product Waves Will Define Meta’s 2026 Strategy

Meta’s AI smart glasses roadmap is rapidly expanding beyond a single product family.

The first wave is represented by today’s launch of Adventurer, Fury, and Starfire Kylie Edition. SAG expects three additional waves during the remainder of 2026.

The second wave is expected this fall with Luna, a new Meta-owned audio AI smart glasses platform designed to further expand Meta’s reach beyond the Ray-Ban ecosystem.

The third wave will likely be a premium luxury co-branded initiative under the code name Mojito VIP, targeting affluent consumers and luxury buyers.

The fourth wave is expected to be the launch of RBM 2 Refresh, an upgraded version of the successful Meta Ray-Ban platform.

Together, these launches represent the broadest AI smart glasses portfolio currently planned by any global technology vendor and demonstrate Meta’s determination to establish a commanding lead before competition intensifies.

A 20 Million Unit Market Is Emerging

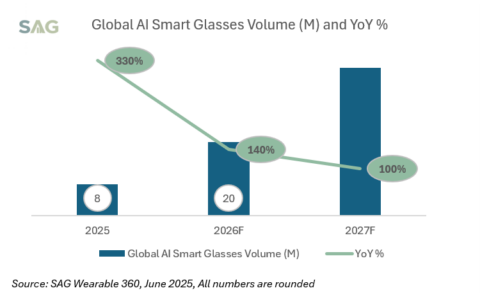

SAG forecasts global AI smart glasses shipments will exceed 20-million-unit milestone in 2026, representing approximately 140% year-over-year growth.

Exhibit 2: Global AI Smart Glasses Volume (M) and YoY %

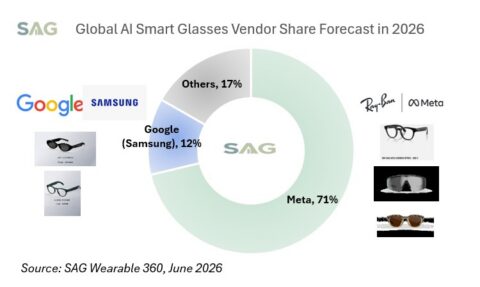

SAG forecasts Meta will remain the dominant market leader, accounting for roughly 71% of global shipments and exceeding 14 million units worldwide in 2026. Google and Samsung are expected to follow with approximately 12% market share combined, surpassing 2 million units.

Exhibit 3: AI Smart Glasses Vendor Share in 2026

The market remains highly concentrated today, but competitive intensity is expected to increase significantly as Google, Samsung, Apple, and leading Chinese brands continue to expand their investments in the category.

Why Is Meta Pushing So Hard?

Meta’s AI investments have reached tens of billions of dollars annually, and the company increasingly needs consumer-facing hardware capable of showcasing and monetizing those investments.

SAG believes AI smart glasses represent the most practical consumer AI device currently available. Unlike smartphones, AI smart glasses offer always-available voice interaction, first-person contextual awareness, hands-free operation, and natural integration into daily life.

At the same time, Meta is attempting to strengthen its leadership position before larger ecosystem competitors gain momentum. Google and Samsung are accelerating their AI smart glasses initiatives this year, while Apple is widely expected to enter the category in 2027.

From Meta’s perspective, 2026 may represent the final opportunity to establish overwhelming scale advantages before the competitive landscape becomes significantly more crowded.

From Technology to Fashion: The Importance of Starfire

Perhaps the most interesting announcement today is not Adventurer or Fury, but Starfire Kylie Edition.

The co-branding partnership with global lifestyle and beauty celebrity Kylie Jenner signals that Meta increasingly views AI smart glasses as a fashion and lifestyle product rather than simply another technology gadget.

SAG believes this is a smart and necessary move.

Unlike smartphones, AI smart glasses are highly visible products worn directly on the face. Consumers evaluate them not only based on specifications and AI capabilities, but also on appearance, personal style, comfort, fashion appeal, and social identity.

In many ways, AI smart glasses have more in common with traditional eyewear, watches, and fashion accessories than with smartphones.

Lifestyle positioning therefore becomes a critical factor in driving mainstream adoption.

This strategy also helps explain why Google and Samsung are partnering closely with established eyewear and fashion brands for their own AI smart glasses initiatives. Technology alone is unlikely to drive mass-market adoption. Successful vendors must combine AI capabilities with attractive design, strong branding, and lifestyle appeal.

It remains to be seen how Apple will approach this challenge when it enters the market, but history suggests Apple understands the importance of blending technology, design, and lifestyle better than most competitors.

Chinese vendors, meanwhile, have made significant progress in hardware innovation and AI integration but generally lag global leaders in branding, fashion marketing, and lifestyle positioning. This remains one of the biggest gaps separating Chinese AI smart glasses vendors from Meta today.

Why Meta Is Moving Beyond Ray-Ban

One of the most notable developments is Meta’s decision to launch AI smart glasses carrying Meta branding rather than the Ray-Ban name.

SAG believes this reflects two strategic priorities. First, Meta increasingly wants consumers to associate AI smart glasses directly with the Meta brand and ecosystem. Second, Meta can potentially reduce licensing-related expenses and improve hardware margins by emphasizing its own branding while continuing to leverage the manufacturing and distribution expertise of EssilorLuxottica.

The new products remain manufactured by EssilorLuxottica and are distributed through Meta’s own channels, Sunglass Hut, LensCrafters, Best Buy, Amazon, and other retail partners.

The products are initially available in 17 countries across North America, Western Europe, and Australia, with additional markets expected to be added throughout the year.

SAG expects Meta-branded AI smart glasses alone, including today’s launches and the upcoming Luna platform, to generate more than 4 million shipments in 2026, representing roughly 30% of Meta’s total AI smart glasses volume. This ratio could approach 40% in 2027 as lower pricing and broader distribution continue to drive adoption.

Outlook: The Race Is Just Beginning

The AI smart glasses market is rapidly transitioning from experimentation to scale.

The next 18 months will be critical. Meta is racing to build scale before Apple arrives. Google and Samsung are preparing their next moves. Chinese vendors are building an increasingly independent ecosystem. Meanwhile, consumer awareness continues to rise worldwide.

Another important industry development is the availability of Qualcomm’s Snapdragon Start platform. SAG believes Snapdragon Start will significantly lower the entry barriers for AI smart glasses and other eyewear wearable products by reducing development complexity, shortening product development cycles, and lowering hardware costs. As a result, more vendors will be able to enter the market over the next several years.

However, easier hardware development does not necessarily translate into commercial success. As the technology platform becomes more accessible and standardized, competitive advantages will increasingly shift away from hardware specifications and toward brand strength, distribution reach, ecosystem integration, software experiences, fashion appeal, and consumer trust.

This trend favors global ecosystem leaders such as Meta, Apple, Google, and Samsung. These companies possess established consumer brands, strong retail and operator partnerships, large developer ecosystems, significant marketing resources, and global distribution networks that are difficult for smaller competitors to replicate.

Meta’s partnership with Kylie Jenner further highlights this shift. The future battle for AI smart glasses will not be won solely through technology. It will increasingly be determined by who can best combine AI capabilities, fashion, lifestyle branding, ecosystem integration, and retail execution.

Chinese brands are making rapid progress in AI capabilities and hardware innovation, but generally remain behind global leaders in branding, fashion marketing, and premium lifestyle positioning. Smaller brands face even greater challenges as competition intensifies and marketing costs rise.

SAG therefore expects the AI smart glasses market to become increasingly concentrated around a handful of global ecosystem leaders over the next three to five years. While smartphones will remain the primary personal computing device, AI smart glasses are emerging as the leading candidate to become the next major interface layer between consumers and AI.