- SAG forecasts global AI smart glasses shipments will grow 85% YoY in 2026, surpassing 15 million units worldwide.

- Audio AI smart glasses will remain the dominant form factor, accounting for an estimated 91% of global shipments in 2026.

- Google’s entry will accelerate category growth and challenge Meta’s dominance, especially by combining Google’s Gemini AI, Android ecosystem, Samsung’s hardware engineering, and eyewear partners’ design and retail strengths.

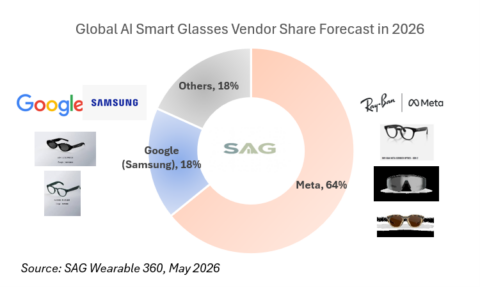

- SAG expects Google AI smart glasses shipments to exceed 2 million units globally in 2026, assuming no major supply constraints or launch delays. This would give Google nearly 18% global market share, ranking it No. 2 worldwide, behind Meta but ahead of Chinese AI smart glasses providers such as Rokid, Xiaomi and Huawei etc.

- Warby Parker and Gentle Monster bring complementary go-to-market advantages. Warby Parker strengthens Google’s North American optical-service and mainstream retail access, while Gentle Monster adds premium fashion credibility, Asian market relevance, and global cultural visibility.

Google today announced its latest AI smart glasses push at Google I/O 2026, showcasing new intelligent eyewear developed with Samsung and designed in partnership with Warby Parker, an American eyewear brand, and Gentle Monster, a Korean eyewear brand. The announcement marks Google’s most serious return to smart eyewear and signals that AI smart glasses are moving closer to mainstream consumer adoption. Google said the new eyewear will combine AI with everyday wearability and support use cases such as directions, messaging, photo capture and hands-free assistance.

Image 1: Google audio AI smart glasses (Gentle Monster and Warby Parker)

Smart Analytics Global (SAG) forecasts global AI smart glasses shipments will grow 85% YoY in 2026, surpassing 15 million units worldwide. The category is moving from early experimentation toward broader consumer adoption, supported by stronger AI use cases, improving hardware design, and expanding ecosystem participation from major technology and eyewear brands.

Within the category, audio AI smart glasses will remain the dominant form factor, accounting for an estimated 91% of global AI smart glasses shipments in 2026. Audio models are likely to scale faster than display-based models because they are lighter, less expensive, easier to design around daily eyewear habits, and less exposed to privacy and regulatory concerns. For most consumers, hands-free voice interaction, camera-assisted AI, translation, messaging, navigation, and content capture will be the first wave of mainstream use cases.

The launch of Google AI smart glasses will further accelerate category growth and bring meaningful competition to Meta’s current dominance. SAG believes Google’s partnership strategy is moving in the right direction. By working with traditional eyewear brands such as Warby Parker and Gentle Monster, as well as with Samsung on the technology and ecosystem side, Google can combine AI, software, Android ecosystem reach, and device know-how with the design credibility, fashion appeal, prescription support, and offline distribution channels of established eyewear players.

The two eyewear partners bring very different but complementary strengths.

Warby Parker is a North American volume and accessibility player, with a dense physical retail footprint across the United States and Canada, a healthcare-oriented store model, and strong capabilities in prescription eyewear, eye exams, contact lens fittings, and standardized retail execution. This makes Warby Parker well positioned to help Google reach mainstream consumers who treat smart glasses as an everyday optical product rather than a fashion statement.

Gentle Monster, by contrast, is a premium, fashion-forward global eyewear brand with a highly curated presence in major cultural and fashion capitals, including South Korea, Mainland China, Tokyo, Bangkok, New York, London, Paris, and Milan. Its immersive flagship stores and art-driven retail concept appeal to younger, style-conscious, premium consumers and can help position Google AI smart glasses as a desirable lifestyle and fashion product, especially across Asia and global luxury retail hubs. Together, Warby Parker gives Google scale and optical-service credibility in North America, while Gentle Monster gives Google premium brand heat, fashion relevance, and stronger exposure to Asian and global trend-setting consumers.

This collaboration model is critical for the AI smart glasses market. Unlike smartphones, eyewear is highly personal, fashion-driven, and fit-sensitive. Consumers do not choose glasses based only on technology specifications. Comfort, style, face fit, prescription lens support, retail fitting experience, and brand trust all matter. Technology companies need eyewear partners to overcome these adoption barriers, while eyewear brands need technology partners to bring AI capability, cloud services, developer ecosystems, and user bases into the product experience.

SAG expects Google AI smart glasses to generate more than 2 million units globally in 2026, assuming no major supply constraints and no launch delay, under a reasonable price tag. This would give Google nearly 18% global market share, ranking it No. 2 worldwide, behind Meta but ahead of Chinese AI smart glasses providers such as Rokid, Xiaomi and Huawei etc.

Exhibit 1: Global AI Smart Glasses Vendor Share Forecast in 2026

Meta will likely remain the clear leader in 2026, supported by its early-mover advantage, Ray-Ban partnership, strong consumer awareness, and expanding AI assistant capabilities. However, Google’s entry could reshape the competitive landscape by bringing Android ecosystem scale, Gemini AI integration, Samsung hardware collaboration, and broader eyewear brand partnerships into the market.

SAG believes 2026 will be a key inflection year for AI smart glasses. The market will still be led by audio-first products, but competition will intensify as major ecosystem players enter the category. The winners will not be determined by AI capability alone. Success will depend on the ability to combine AI, hardware, fashion, prescription support, retail distribution, and consumer trust into a wearable product that people are willing to use every day.