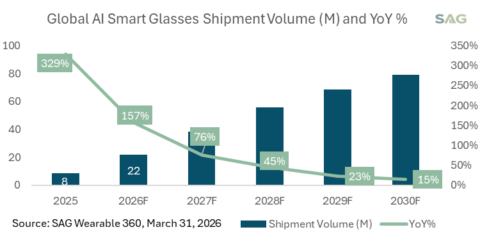

The AI smart glasses market reached an important milestone in 2025, but 2026 will be the year when the industry truly begins to scale.

Smart Analytics Global (SAG) tracked global shipments reached 8.5 million units in 2025, growing 330% YoY. SAG expect the strong momentum will maintain, with shipment volumes growing 157% YoY to 22 million units, and trade wholesale revenue surging 178% YoY to US$6 billion.

Meta’s continued ramp-up and extended product lineup, as well as the entry of Samsung and Google marks a major shift, signaling that AI smart glasses are moving from an experimental category into a mainstream consumer electronics segment.

Exhibit 1: Global AI Smart Glasses Shipment Volume (M) and YoY %

Big Tech Entry Reshapes the Competitive Landscape

The competitive landscape is entering a new phase. Meta remains the clear leader today, supported by its early success and strong ecosystem. However, from 2026 onwards, Samsung and Google will begin to build scale, followed by Apple in 2027. This will reshape the market into a structure led by a few global brands. SAG expects Meta, Apple, and Samsung to emerge as the top three players over time, while smaller vendors gradually lose share or move into niche segments, similar to what happened in the smartphone market.

Two Product Paths: Audio Leads, HUD Drives Value

The market is evolving along two product paths. Audio smart glasses continue to dominate in volume because they are more affordable and easier to use. However, the real value growth is coming from HUD smart glasses. These devices are improving quickly, moving from single-eye displays to dual-eye designs and from simple green displays to full-color experiences. Their use cases are also expanding, from basic notifications to navigation and real-time assistance. Even so, HUD glasses remain different from true AR devices, as they do not fully anchor digital content into the real world.

Why HUD Will Grow but Not Dominate

Despite strong momentum, HUD smart glasses will remain a secondary category in the next few years. Their higher cost and pricing make it harder to reach mass adoption, and supply constraints, especially for early products like Meta’s display models, may slow the rollout. Regulatory risks are another factor. In Europe, privacy concerns under GDPR have already delayed approval of display-enabled devices, and similar issues are likely to emerge in Japan and parts of the Middle East. These challenges will limit how fast HUD glasses can scale, even though their share will increase steadily over time.

Regional Differences Will Shape Adoption

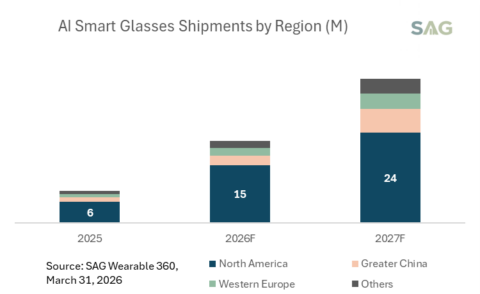

Regional dynamics will continue to play a major role. North America will remain the largest and most valuable market, driven by strong demand for premium products. China will scale quickly but remain more price-sensitive, with strong competition among local vendors. In Europe and Japan, adoption may be slower due to regulatory and cultural concerns. In emerging markets, growth will depend heavily on distribution, which is still developing.

Exhibit 2: AI Smart Glasses Shipments by Region

Distribution and User Experience Are the Real Bottlenecks

Unlike smartphones, smart glasses combine technology, fashion, and eyewear, which makes distribution more complex. Consumers often want to try them before buying, so offline channels such as eyewear stores and electronics retailers are critical. In markets where these channels are less developed, adoption may be slower. At the same time, user experience still needs improvement. While music, video, and hands-free interaction are popular, users continue to face issues with battery life, limited apps, and bulky designs, per the Meta Ray-ban Display user benchmark report from UXConnect. Voice commands can be inconsistent, and gesture controls are not always intuitive. Improving UI and overall user experience will be key to reducing friction and driving long-term adoption.

SAG Takeaway

SAG believes the AI smart glasses market will grow rapidly through 2030, but the path will not be smooth. Audio smart glasses will remain dominant in volume, while HUD devices will drive most of the revenue growth. The entry of Samsung and Google in 2026 / Apple in 2027 will mark the start of a new phase, where scale, ecosystem strength, and user experience will determine long-term winners.

Clients please click here to access the comprehensive report, covering AI smart glasses shipments, trade wholesale ASP and revenue by major vendors by type across 14 regions / countries from 2024 through 2030.