The report that OpenAI may be developing its own smartphone platform, potentially in partnership with Qualcomm, MediaTek and Luxshare Precision, has quickly fueled debate over what the next generation of AI hardware could look like. The rumor, highlighted by Apple supply chain analyst Ming-Chi Kuo, should not be treated as a random experiment. In fact, from a long-term platform perspective, the logic is highly understandable.

If OpenAI truly wants to build a durable hardware gateway for the AI era rather than remain a software layer dependent on other ecosystems, smartphones are the one category it cannot ignore.

Smartphones Still Sit at the Center of Consumer Electronics

Despite the rise of wearables, AI glasses, earbuds, and other connected devices, smartphones remain the undisputed center of personal computing and daily digital engagement.

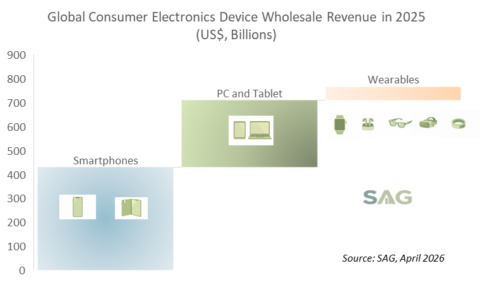

According to Smart Analytics Global (SAG), global trade wholesale revenue across smartphones, PCs, tablets, and wearables reached approximately US$770 billion in 2025. Smartphones alone contributed more than 55% of that total, followed by PCs at over 31%, while tablets and wearables each represented slightly above 7%.

Exhibit 1: Global Consumer Electronics Device Trade Wholesale Revenue in 2025 (US$, Billions)

No other personal device category combines this level of shipment scale, user stickiness, service attachment opportunity, and monetization visibility.

This is precisely why OpenAI’s broader hardware preparations deserve attention. The company has already built a dedicated hardware effort under former Apple design chief Jony Ive, while separate reports suggest it is also exploring a TWS earbud product under the codename Sweetpea. But earbuds alone are too small to become the main AI hardware anchor. By revenue, the global TWS market is only around 5% of smartphone market size. It can serve as an AI companion, but not the primary consumer interface.

For any AI platform provider trying to secure long-term consumer relevance, smartphones remain the largest and most strategic prize.

Strategic Rationale Is Clear, but Commercial Execution Will Be Extremely Difficult

This is where the OpenAI smartphone story becomes much less straightforward.

The smartphone business is not an open field waiting for disruption and newcomers. It is one of the most mature, concentrated, and operationally difficult hardware industries in the world.

Apple, Samsung Electronics and leading Chinese vendors have spent more than a decade building deep control over supply chains, operator relationships, retail channels, hardware-software optimization, and marketing ecosystems. According to SAG estimates, Apple and Samsung together generated roughly 70% of global smartphone trade wholesale revenue in 2025 and captured more than 95% of the industry’s operating profit pool.

That leaves very little room for a newcomer, even one carrying the OpenAI name.

Smartphone industry is a replacement-driven, highly consolidated business where incumbents already own the premium customer base, the channel shelf space, and the profit structure.

Breaking into this market is not simply about launching a good AI phone. It means displacing some of the most deeply entrenched hardware franchises in consumer technology.

AI Still Is Not a Proven Smartphone Replacement Driver

One of the biggest assumptions behind the AI phone narrative is that consumers are waiting for AI to trigger the next major smartphone upgrade cycle.

SAG does not believe the data supports that view.

Our consumer research continues to show that the leading purchase factors for smartphones remain camera performance, display quality and size, battery life, memory configuration, and pricing. AI functionality still ranks well below these core hardware attributes. In the US market specifically, only around 10% of consumers currently show strong willingness to prioritize AI features when choosing a new smartphone.

This matters because OpenAI cannot rely on AI branding alone to generate immediate mainstream pull.

In fact, across the premium smartphone segment, agentic AI-capable chipsets and supporting software frameworks have already become widely deployed. Among smartphones carrying a wholesale ASP above US$600, both on-device and cloud-connected AI stacks are increasingly standard hardware infrastructure rather than a unique point of differentiation.

In other words, the premium smartphone market does not lack AI-ready silicon. It lacks AI experiences compelling enough to materially change consumer behavior and replacement behavior.

That is a very different challenge.

Consumers Want Smarter Phones, Not Phones That Take Too Much Control

There is another issue that hardware specifications alone cannot solve: consumer trust.

Many AI platform companies envision a future where generative AI gradually replaces app-centric workflows and becomes the dominant interface layer on personal devices. The theory is simple: fewer apps, fewer taps, more automation.

The consumer reality is far more complicated.

Early AI-centric smartphone trials in China, including Doubao-linked implementations, have already shown visible hesitation when AI becomes too intrusive, too autonomous, or too aggressive in trying to manage user behavior. Consumers may appreciate AI assistance, but they still want to remain in control of how their smartphone operates.

This creates a major caution point for OpenAI.

Image 1: App Smartphone UI vs. Agentic Smartphone UI (source: Ming-Chi Guo X account)

An OpenAI-branded phone would naturally carry heightened scrutiny around privacy, data security, and the broader concern that AI could become overly embedded in personal decision-making. The more AI attempts to replace human control, the more trust becomes fragile.

This is also why SAG believes Samsung Electronics is currently taking the more realistic path with its Galaxy S26 AI roadmap. Rather than trying to force a radical interface reset, Samsung is layering AI gradually through collaboration with Google and major app partners, improving workflows step by step while keeping users inside familiar operating patterns.

For mainstream consumers, that measured migration path is likely much easier to accept.

Qualcomm and MediaTek Can Help, but They Cannot Create Sustainable Differentiation

The reported involvement of Qualcomm and MediaTek sounds strategically attractive, but it should be viewed with realism.

Neither chipset supplier is likely to commit a highly exclusive silicon roadmap for OpenAI given the uncertain shipment outlook and the significant risk profile of any new smartphone entrant. More importantly, premium Android vendors have already moved aggressively to adopt AI-ready processors and software stacks across flagship and upper-mid tiers.

This means OpenAI may gain marketing value by aligning with AI-leading silicon suppliers, but not necessarily a defensible hardware differentiator.

At this point, AI-capable smartphone hardware is no longer rare. It is rapidly becoming table stakes.

The real industry bottleneck is no longer chipset readiness. It is meaningful user differentiation.

And that remains far harder to solve.

OpenAI Understands the Need for Hardware, but Smartphones Remain the Most Difficult Entry Point

SAG believes OpenAI’s rumored smartphone initiative reflects a broader strategic realization: leadership in AI software alone may not be sufficient to secure long-term consumer influence if the primary hardware gateways remain controlled by incumbent device vendors.

That strategic thinking is understandable.

AI platform leaders do not want to remain permanently dependent on Apple, Google, Samsung Electronics, or other ecosystem owners for hardware distribution, user traffic entry, and data interface control. Building some level of direct hardware presence is therefore a logical next step if OpenAI wants to preserve its long-term relevance beyond the software layer.

However, recognizing the need for hardware and successfully establishing a smartphone business are two very different challenges.

Among all AI-related device categories, smartphones remain the most difficult segment to penetrate because of their mature competitive structure, high supply chain complexity, entrenched operator and retail relationships, and extremely concentrated profit pool. Building a smartphone brand entirely from the ground up would require not only major capital commitment, but also years of channel cultivation, manufacturing optimization, after-sales support, and consumer trust building.

By contrast, other AI hardware categories such as TWS earbuds and AI smart glasses offer lower barriers to experimentation, faster product cycles, and less entrenched competitive dynamics, even though they cannot match smartphones in market size or ecosystem importance. These categories may provide more manageable platforms for OpenAI to test AI-centric interaction concepts before taking on the significantly more complex smartphone market.

Acquisition May Be the More Realistic Shortcut Than Building a Smartphone Brand from Scratch

If OpenAI is serious about establishing a smartphone hardware presence, SAG believes acquisition or strategic control of an existing smartphone player would likely be a more realistic path than attempting to build a new branded handset business entirely from zero.

The smartphone industry is not a category where software strength alone can quickly translate into shipment scale. Existing OEM infrastructure matters heavily, including manufacturing resources, carrier certifications, component sourcing relationships, regional compliance, retail execution, and post-sales service capability. Acquiring these capabilities through an established player would significantly shorten development cycles and reduce operational uncertainty.

Such a route would also allow OpenAI to focus its internal resources on what it does best: AI interface design, cloud intelligence integration, and ecosystem-level software differentiation, rather than spending years rebuilding mature hardware fundamentals already mastered by incumbent smartphone vendors.

This is not to suggest that suitable acquisition targets are easy to find. Most leading smartphone brands are either too large, too strategically protected, or too deeply integrated into broader conglomerate structures. However, the broader conclusion remains valid: entering smartphones through partnership, investment, or acquisition-led control is operationally far more feasible than attempting a clean-sheet market entry.

This also echoes SAG’s broader view on the current market debate surrounding Apple’s AI position. The industry may be overreacting to Apple’s near-term AI software gap. Smartphones are fundamentally different from PCs, where AI can more directly influence productivity-led replacement demand. In smartphones, replacement behavior remains far more conservative, giving Apple meaningful time to work with external AI partners, refine its software roadmap, and gradually extend intelligence across a broader hardware portfolio.

The same lesson applies to OpenAI from the opposite direction: strong momentum in AI software does not automatically translate into success in consumer hardware.

Hardware remains a business defined by scale, execution discipline, channel power, and consumer trust.

And nowhere is that barrier higher than in smartphones.