President Trump’s visit to China this week, joined by a high-profile group of U.S. technology and business leaders including Tim Cook, Elon Musk, Jensen Huang and other major tech CEOs, sends an important signal to the global technology sector: dialogue between the world’s two largest economies is reopening at a critical moment.

For the tech industry, this matters. The U.S. and China remain fierce competitors in AI, semiconductors, smartphones, EVs, robotics, cloud infrastructure and next-generation computing platforms. But they are also deeply connected through markets, manufacturing, components, capital, talent and supply chains. Any improvement in the tone of U.S.-China relations is therefore good news not only for the technology sector, but also for the broader global economy.

Dialogue Is Back, and Tech Needs It

The visit does not mean U.S.-China tensions will disappear. Export controls, national security reviews, tariff risks, AI regulation and supply-chain localization will remain. However, reopening a dialogue window is still meaningful.

For technology companies, investors, suppliers and consumers, the biggest risk is uncertainty, policy shocks and prolonged standoff between the two largest economies. A more constructive U.S.-China dialogue can help reduce volatility and give companies more room for long-term planning.

SAG believes the improved tone between the U.S. and China is a positive signal. It does not remove geopolitical risk, but it helps create a more stable environment for global technology supply chains, market access and investment decisions.

AI Chips Are Now the Center of Tech Diplomacy

One of the most important themes of this visit is AI. Nvidia’s H200 AI chipset export into China has become a key focus point, reflecting the broader tension between AI competition and AI regulation.

For Nvidia, China remains one of the largest potential AI infrastructure markets globally. Demand for advanced AI accelerators remains strong across cloud service providers, enterprise AI, model training and digital infrastructure. For China, access to advanced AI chips can help accelerate AI deployment, even as the country continues to invest heavily in domestic semiconductor alternatives.

Both the U.S. and China are trying to balance innovation, market access, national security and regulatory control. This makes the H200 discussion much bigger than one chipset. It reflects the future direction of global AI competition.

The U.S. and China will continue to compete aggressively in AI. The real question is whether the two countries can compete while still maintaining communication on rules, boundaries and risk management. AI competition is not only about chips. It also includes cloud infrastructure, foundation models, data governance, enterprise deployment, safety standards, energy availability and cross-border regulation.

SAG believes AI competition between the U.S. and China will remain intense, but dialogue is necessary. Without communication, companies face higher uncertainty, fragmented standards and greater supply-chain disruption. With communication, competition can remain tough but more manageable.

China Remains Essential to Apple’s iPhone Business

For Apple, Tim Cook’s presence during the visit delivered one message: China remains critically important to Apple’s global business.

China is not only a manufacturing base for Apple. It is also one of Apple’s most important consumer markets, a key premium smartphone battleground and a major ecosystem market for iPhone, services, wearables and future AI-enabled devices.

Taking iPhone as an example, Smart Analytics Global (SAG) estimates that China is now the second-largest single-country market for iPhone shipments globally. SAG expects China to account for 19% of global iPhone volume in 2026, up from 18% in 2025.

The iPhone 17 series have continued to ramp volumes in China and remains among the top-selling smartphone model families since later last year. Despite strong competition from Huawei, Apple continues to benefit from strong premium brand equity, a sticky iOS ecosystem and resilient demand among higher-income Chinese consumers.

SAG expects the upcoming foldable iPhone to further strengthen Apple’s competitive position in China. China is the world’s largest foldable smartphone market and contributed more than half of global foldable smartphone shipment volume in 2025, according to SAG’s smartphone 360 service. This makes China a critical market for Apple’s foldable strategy.

Chinese vendors have already educated consumers on foldable use cases, pricing, retail experiences and form-factor innovation. If Apple delivers a refined user experience, strong app compatibility, premium industrial design and a differentiated wide-fold form factor, the foldable iPhone could become an important growth catalyst in China’s premium smartphone segment.

Apple Is Diversifying, But China Is Still Hard to Replace

Apple has been shifting part of its iPhone manufacturing footprint from China toward India in recent years, driven by tariff risk, cost factors and geopolitical uncertainty.

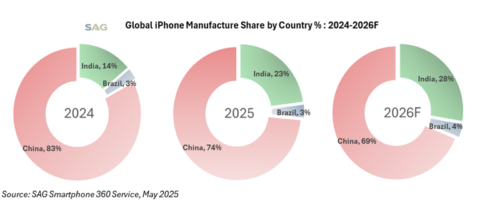

SAG estimates that China still dominated global iPhone manufacturing in 2025 with a 74% volume share, down from 83% in 2024. India’s share surged from 14% in 2024 to 23% in 2025, and SAG expects India’s share to further rise to 28% in 2026.

Exhibit 1: iPhone Manufacture Country Share: 2024-2026F

This diversification trend will continue. India is becoming an increasingly important iPhone production hub, supported by Apple’s supply-chain partners (Foxconn and Tata group etc.), local policy support (PLI scheme) and growing manufacturing capability.

However, it will be very difficult for India or any other country to fully replace China in the near term. China still holds major advantages in iPhone manufacturing, including supply-chain density, mature labor and engineering ecosystems, component supplier proximity, logistics efficiency, production flexibility and decades of accumulated manufacturing know-how.

Many key component suppliers and manufacturing partners remain deeply rooted in China. The ability to scale production quickly, manage complex product transitions and coordinate across hundreds of suppliers remains a major advantage for China.

India will continue to gain share, but China is likely to remain the backbone of global iPhone production for the foreseeable future. Apple’s strategy is more about building a more balanced, resilient and flexible global manufacturing network.

SAG View: Less Uncertainty Is Good News for Global Tech

A more constructive U.S.-China relationship matters greatly for Apple and the broader technology industry.

Apple needs China as both a market and a manufacturing hub. China also benefits from Apple’s continued investment, supply-chain employment, retail presence, developer ecosystem and role in sustaining premium consumer electronics demand.

The same logic applies more broadly across the tech sector. Nvidia, Tesla, Apple, Qualcomm, Microsoft, Google, Amazon and many other technology companies all have important exposure to China, either through demand, supply chain, manufacturing, developers or ecosystem partnerships.

However, we should remain realistic. One visit or one summit will not erase years of geopolitical tension. The U.S. and China will continue to compete in AI, semiconductors, smartphones, EVs, robotics, cloud computing and next-generation platforms. Export controls and regulatory reviews will remain part of the landscape.

However, the direction of travel matters. A world where the two largest economies keep talking is better than a world defined only by standoff, escalation and rivalry.