Key Takeaways

• Oura today launched Ring 5 with major hardware upgrades, including a significantly slimmer form factor, longer battery life, additional color options, and broader language support.

• Ring 5 weight has been reduced to just 2g, compared with 5-6g for Ring 4.

• Thickness has been reduced from 3.51mm to 2.28mm, while width has narrowed from 7.9mm to 6.09mm.

• Battery life has been extended to 6-9 days, compared with 5-8 days on Ring 4.

• Oura expanded local language support to include Chinese, Hindi, Korean, Polish, and Portuguese, increasing its addressable user base across multiple regions.

• Ring 5 is priced at US$399, slightly higher than Ring 4 but below SAG expectations.

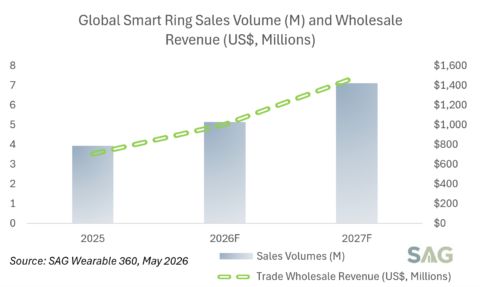

• SAG forecasts global smart ring shipments will exceed 5 million units in 2026 and 7 million units in 2027, generating trade wholesale revenue of approximately US$1.0 billion and US$1.5 billion, respectively.

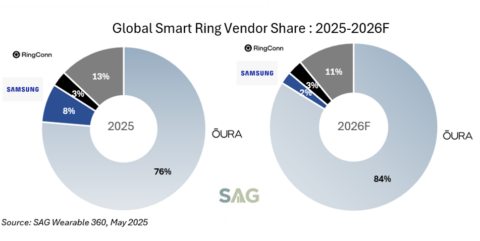

• Oura is expected to maintain market leadership with approximately 84% share in 2026 and 70% share in 2027.

• The smart ring market remains niche compared with smartwatches, but its growth highlights an important shift in consumer behavior toward lighter, less disruptive wearable experiences.

Oura Ring 5 Focuses on the Biggest Wearable Pain Point: Less Is More

The most significant upgrade of Oura Ring 5 is the dramatically slimmer and lighter hardware design.

Ring 5 reduces weight to just 2g, compared with 5-6g on Ring 4. Thickness has been cut from 3.51mm to 2.28mm, while width has narrowed from 7.90mm to 6.09mm. At the same time, Oura expanded color choices from three options on Ring 4 to six options on Ring 5.

Exhibit 1: Oura Ring 5 Image

SAG believes these changes directly address one of the largest barriers to wearable adoption: users simply do not want to feel the device they are wearing.

According to SAG consumer research, lightweight design and less disruption consistently rank among the top pain points for wearable users, alongside battery life, accuracy, and comfort. By significantly reducing the physical footprint of the device while extending battery life, Oura has addressed a critical consumer demand that many wearable vendors continue to overlook.

Longer Battery Life and More Languages Expand the Addressable Market

Beyond hardware improvements, Oura also extended battery life from 5-8 days to 6-9 days, further reducing charging frequency and improving the overall ownership experience.

The company additionally introduced support for Chinese, Hindi, Korean, Polish, and Portuguese, substantially expanding the product’s addressable market.

SAG believes localization remains one of the most underappreciated growth drivers in wearable technology. The addition of these languages enables Oura to better address users across Asia, Latin America, and parts of Europe, supporting future international expansion beyond its traditional North American and Western European strongholds.

Why Non-Display Wearables Are Gaining Momentum

The success of Oura and the rapid growth of Whoop point to a broader industry trend.

Consumers are increasingly seeking wearable experiences that are less intrusive and less distracting than traditional smartwatches.

Unlike smartwatch displays that constantly compete for user attention, smart rings and non-display bands focus on passive data collection, wellness tracking, and personalized insights. This approach aligns with a growing segment of consumers seeking health benefits without adding another screen to their daily lives.

SAG expects this trend to accelerate over the coming years as wearable products continue evolving toward more ambient, lightweight, and invisible computing experiences.

The growing popularity of smart rings and non-display bands demonstrates that the future of wearables is not necessarily about adding more displays, but often about reducing them.

The Subscription Debate: Hardware Only or Hardware Plus Services?

One of the most interesting strategic questions in the wearable industry remains the business model.

Unlike Whoop, which requires an ongoing annual subscription, Oura continues to offer hardware-only purchases while providing users with a one-month free trial of its premium services.

Notably, more than 60% of Oura smart ring buyers have reportedly converted into subscribers following purchase.

SAG believes there is no universal answer regarding which business model is superior.

For premium users, combining hardware and subscription services can significantly improve user experience, increase customer stickiness, strengthen brand loyalty, and create competitive differentiation through proprietary insights and services. Subscription revenue also tends to carry substantially higher margins than hardware revenue.

However, mandatory subscriptions can create adoption barriers for mainstream consumers.

Hardware-only models lower consumer hesitation and reduce purchase friction, making them more suitable for mass-market adoption. The challenge is that hardware businesses often face greater pricing pressure, lower recurring revenue, and higher customer churn.

Ideally, consumers should have the flexibility to choose the model that best fits their needs. SAG believes Google Fitbit Air represents a compelling example of this approach by providing more options and lower barriers to entry for consumers.

Smart Rings Remain Niche but Growth Is Difficult to Ignore

While smart rings remain significantly smaller than the smartwatch market, the growth trajectory is becoming increasingly difficult to ignore.

SAG forecasts global smart ring shipments will surpass 5 million units in 2026 and reach approximately 7 million units in 2027. Trade wholesale revenue is expected to grow to roughly US$1.0 billion in 2026 and US$1.5 billion in 2027.

Exhibit 2: Global Smart Ring Volume and Wholesale Revenue and YoY % Forecast

Oura is expected to maintain its dominant market position with approximately 84% market share in 2026 and 70% in 2027, although competition is likely to intensify as additional vendors enter the category.

Exhibit 3: Smart Ring Vendor Market Share: 2025 – 2026F

The segment remains small today, but its rapid growth reflects a broader evolution in wearable technology and changing consumer preferences toward lighter, more comfortable, and less disruptive devices.

Apple, Samsung and the Next Wave of Competition

Looking ahead, the most important question for the smart ring industry is about whether major ecosystem players decide to enter the category.

Apple and Samsung remain the two companies that industry stakeholders are watching most closely. Both companies possess significant ecosystem advantages, brand power, distribution networks, and health platform capabilities that could rapidly accelerate category awareness and adoption.

Whether through smart rings, non-display bands, AI-powered wellness devices, or other emerging form factors, SAG believes the wearable industry is rapidly evolving and entering a new phase where comfort, simplicity, and passive intelligence increasingly matter more than adding another screen.