- Oura’s confidential IPO filing marks a validation moment for smart rings, signaling the category’s shift from a niche wellness device to a more investable and strategically important wearable segment.

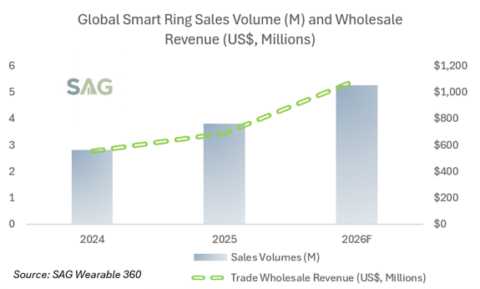

- SAG Wearable 360 tracked global smart ring sales volume at 3.8 million units in 2025, up 36% YoY, while trade wholesale revenue approached US$700 million, up 25% YoY.

- SAG expects smart rings to cross two key milestones in 2026: global sales volume reaching 5 million units and trade wholesale revenue reaching US$1 billion, growing 38% YoY and 59% YoY, respectively.

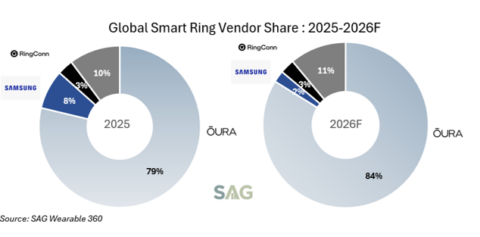

- Oura remains the clear market leader, with its global volume share forecast to rise from 79% in 2025 to 84% in 2026, supported by strong North American demand, channel expansion, and recurring subscription services.

- RingConn is expected to replace Samsung as the No. 2 vendor in 2026, while Samsung’s share is forecast to decline due to the lack of a refreshed model this year. However, Samsung is expected to launch a new smart ring in 2027 and remains well positioned to regain the No. 2 spot.

Smart Rings Move from Niche to Investable Wearable Category

Oura’s confidential IPO filing marks an important milestone for the smart ring market. It is a strong signal that smart rings are evolving from a niche wellness product into one of the most investable and strategically important sub-categories in wearables.

According to Smart Analytics Global’s Wearable 360 service, global smart ring sales volume reached 3.8 million units in 2025, growing 36% YoY. The industry also maintained double-digit growth by value, with trade wholesale revenue approaching US$700 million, up 25% YoY. SAG expects the category to continue expanding rapidly in 2026, with global smart ring sales volume reaching the 5 million unit mark, up 38% YoY, while trade wholesale revenue is forecast to reach the US$1 billion mark, up 59% YoY.

Exhibit 1: Global Smart Ring Sales Volume (M) and Trade Wholesale Revenue (US$, Millions)

This growth trajectory is particularly notable because smart rings remain at an early adoption stage compared with mature wearable categories such as smartwatches, fitness bands and TWS earbuds. While those larger segments remain important in volume terms, their growth rates have normalized. By contrast, smart rings and AI smart glasses are emerging as two of the fastest-growing sub-categories within the broader wearable market.

Oura Strengthens Leadership as Samsung Takes a Pause

Oura remains the clear market leader. SAG estimates Oura’s global smart ring volume share will rise from 79% in 2025 to 84% in 2026, further strengthening its leadership position.

RingConn is expected to replace Samsung as the No. 2 vendor in 2026, with around 3% global market share, supported by active product launches and market expansion. Samsung’s share, by contrast, is forecast to decline from 8% in 2025 to 2% in 2026, mainly due to the lack of a refreshed smart ring product this year.

Exhibit 2: Global Smart Ring Vendor Market Share : 2025-2026F

However, SAG expects Samsung to launch a new smart ring in 2027. The company remains well positioned to regain the No. 2 spot, supported by its Galaxy ecosystem, global channel reach, brand recognition and ability to bundle smart ring experiences with smartphones, smartwatches and broader Samsung Health services.

For Samsung, the near-term challenge is product cadence. The Galaxy Ring helped validate the category in 2025 by bringing a major consumer electronics brand into the market. But without a refreshed model in 2026, Samsung risks losing momentum to more focused smart ring vendors such as Oura and RingConn.

North America Remains the Core Growth Engine

North America remains the largest regional market for smart rings, accounting for over 70% of global volume share, followed by Europe. The region provides a favorable environment for Oura and other smart ring vendors for several reasons.

First, North American consumers are more familiar with monthly subscription models, particularly across health, fitness, wellness and digital services. While subscription fees can still be a hurdle for mass adoption, consumers in the region are generally more willing to pay for recurring services if the perceived health value is strong.

Second, the availability of HSA and FSA accounts in the US helps lower the effective hardware purchase cost for eligible consumers. This creates an affordability lever that is less visible in many other regions, especially for premium smart rings positioned around health, sleep, recovery and preventive wellness.

Third, North America has become the most receptive market for health-first, low-distraction wearables. After COVID, consumers have become more focused on sleep quality, recovery, stress management and continuous health tracking. At the same time, many users are showing signs of screen fatigue. Smart rings fit well into this trend because they offer passive health tracking without adding another display to daily life.

Minimalist Wearables Are Gaining Momentum

The rise of smart rings is part of a broader shift toward minimalist and less intrusive wearable experiences. Not every successful wearable needs to be screen-centric. For some users, the most attractive device is one that quietly collects health data in the background, delivers actionable insights through an app, and avoids the notification overload associated with smartwatches.

This trend can also be seen in the rising momentum of non-display wearable bands, such as Whoop in North America. Both smart rings and non-display bands reflect a similar consumer preference: health tracking, recovery insights and coaching matter more than having another screen on the body.

SAG believes this shift will continue to benefit smart rings, especially among users who want continuous tracking but do not want to wear a smartwatch during sleep or throughout the full day.

China Remains a Challenging Market for Smart Rings

The smart ring market is not growing evenly across regions. Demand in China remains tepid. SAG believes Chinese consumers have not fully embraced the smart ring concept, especially for health tracking.

Smartwatches and fitness bands continue to dominate wearable usage in China, supported by strong local ecosystems, aggressive pricing, rich display-based features and established consumer habits. In this market, smart rings still face challenges around perceived utility, comfort, sizing, pricing and the lack of a clear replacement or complementary use case versus existing wrist-worn devices.

This regional gap highlights an important point: smart rings are not simply a global plug-and-play category. Adoption depends heavily on consumer behavior, health-service awareness, retail education, pricing structure and ecosystem integration.

Channel, Fit and Health Trust Will Define the Next Phase

Oura’s success reflects more than early-mover advantage. SAG believes the company has benefited from a strong foothold in North America, steady channel expansion, focused health and wellness positioning, and a business model that combines hardware revenue with recurring subscription services.

Smart rings are also more complex to sell than many other consumer electronics products. Sizing, fit, comfort and return policies matter more than in categories such as TWS earbuds or smartwatches. As the category scales, vendors with stronger retail presence, sizing tools, after-sales support and health-service partnerships are likely to gain an advantage.

The next phase of competition will move beyond hardware design. Sensors, battery life, comfort and industrial design remain important, but differentiation will increasingly come from software, AI coaching, health insights, subscription services, ecosystem integration and partnerships with healthcare, fitness and insurance players.

Oura’s path shows that smart rings can become more than a device category. They can become a recurring health engagement platform.

SAG View: Smart Rings Are Entering a New Growth Phase

SAG believes Oura’s IPO filing should be viewed as a category validation moment. The smart ring market is still small compared with smartwatches and TWS earbuds, but it is growing faster, attracting stronger investor attention, and building a clearer value proposition around health, sleep, recovery and low-distraction wearable experiences.

In 2026, the smart ring market is expected to cross two important thresholds: 5 million units in global sales volume and US$1 billion in trade wholesale revenue. These milestones will not make smart rings a mass-market category overnight, but they will confirm that the segment has moved well beyond the experimental stage.

SAG Wearable 360 service will soon publish its Smart Ring Vendor and Regional Market Share Tracking & Forecast Report, covering both volume share and value share by vendor and region.

The report will provide high-granularity insights into smart ring market dynamics, competitive positioning, regional demand patterns, and future growth outlook.

Stay tuned for more details from Smart Analytics Global.