Key Takeaways

- iPhone 17 Series was the world’s best-selling smartphone family in Q1 2026, capturing 15% global smartphone shipment share.

- Samsung A Series grew 13% YoY despite weakness in the broader mass-market segment.

- Premium smartphones continued to outperform amid rising BOM and memory costs.

- Galaxy S26 Ultra remained one of the world’s top-selling flagship models despite a delayed launch cycle.

Smart Analytics Global (SAG)’s smartphone 360 service tracked that the world’s top ten smartphone families together accounted for 63% of global smartphone shipment volume in Q1 2026, underscoring the continued concentration of demand around a small group of high-scale product lines.

Within the top ten list, Apple, Samsung and Xiaomi each captured two positions, while vivo (iQOO), OPPO, Honor, and Lenovo-Motorola each secured one slot. The top five product families in Q1 2026 were the iPhone 17 series, Samsung A series, Xiaomi Redmi series, Samsung Galaxy S series, and iPhone 16 series.

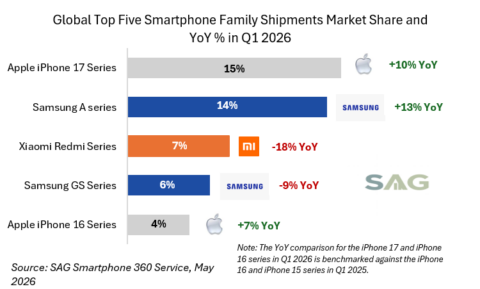

Exhibit 1: Global Top Five Smartphone Family Shipments Market Share and YoY % in Q1 2026

iPhone 17 Series Leads a Resilient Premium Segment

The iPhone 17 Series ranked as the world’s No. 1 smartphone product family in Q1 2026, capturing 15% global shipment volume share. Compared with the iPhone 16 Series in Q1 2025, the iPhone 17 Series delivered roughly 10% YoY growth, highlighting Apple’s continued strength in the premium segment.

At the individual model level, iPhone 17 Pro Max, iPhone 17, and iPhone 17 Pro swept the top three positions globally. The iPhone 17 Series maintained strong momentum across multiple markets, supported by stable pricing and a favorable product mix. While many Android vendors raised prices in response to rising memory and broader BOM costs, Apple largely held iPhone pricing steady, making the iPhone 17 Series more competitive in the current inflationary component environment.

Samsung Galaxy S Series ranked fourth among global smartphone product families, with 6% shipment volume share. It was the other premium product line in the global top ten family list. Galaxy S Series shipments declined 9% YoY in Q1 2026, mainly due to a later launch cycle, as the Galaxy S26 Series launched roughly one month later than the Galaxy S25 family last year.

Despite the delayed launch, Galaxy S26 Ultra still ranked fifth among all individual smartphone models globally, confirming that premium demand remained solid. Consumers in the premium segment are relatively less price-sensitive, while vendors also have wider margins and greater room to absorb BOM cost increases without immediately passing the full burden to consumers.

Samsung A Series Stands Out in a Contracting Mass-Market Segment

Samsung A Series was the world’s second best-selling smartphone product family in Q1 2026, capturing 14% global shipment volume share and growing 13% YoY. This was a notable performance at a time when most other mass-market-oriented product lines were under pressure.

Samsung A Series had multiple models across entry and mid-tier segments in the global best-selling model list. Galaxy A17, A56, and A16 all ranked among the top ten global smartphone models in Q1 2026. Samsung’s strong supply chain position, scale advantages, and portfolio breadth gave the company pricing flexibility that few competitors could match in the current cost environment.

By contrast, most other mass-market product lines in the top ten family list posted declines. Xiaomi Redmi Series and OPPO A Series recorded double-digit YoY shipment declines, while Lenovo-Motorola G Series and vivo Y Series declined by single digits.

Rising memory and component costs are putting disproportionate pressure on mass-market-oriented products, where vendors operate with thinner margins and have less room to absorb cost increases. This divergence within the mass-market segment is likely to widen as BOM cost increases feed more fully into retail pricing from Q2 2026 onward.

SAG Takeaway

The Q1 2026 best-selling smartphone family data points to a market that is increasingly diverging in two directions. Premium products are holding up well, supported by stronger consumer purchasing power, resilient replacement demand, and vendors’ ability to absorb cost pressure. The mass-market segment, however, is facing more visible headwinds as rising component costs squeeze margins and weigh on affordability.

Samsung A Series stands out as a rare exception in the mass-market segment, supported by Samsung’s supply chain strength, product scale, and broad portfolio coverage. SAG expects the premium-versus-mass-market divergence to deepen further in the coming quarters as memory and component cost increases continue to flow through the smartphone value chain.

For a deeper look at global best-selling smartphone product families and models, including five quarters of data across the Top 30 families and Top 300 models, please see SAG’s latest report: SAG Smartphone Top Selling Product Family and Model Intelligence: Q1 2026.