The global smartphone industry entered a clearer premiumization phase in the first quarter of 2026, as market value growth increasingly detached from shipment performance and migrated materially toward higher-priced devices.

According to Smart Analytics Global (SAG) Smartphone 360 tracking, Q1 2026 marked a visible turning point from the traditional smartphone price-tier polarization pattern seen over the past several years. Historically, the market often found resilience at both ends of the spectrum — premium flagship devices on one side and affordable mass-market smartphones on the other. In Q1 2026, however, that dual-engine structure weakened materially, with industry value increasingly moving in one direction toward premium and ultra-premium devices.

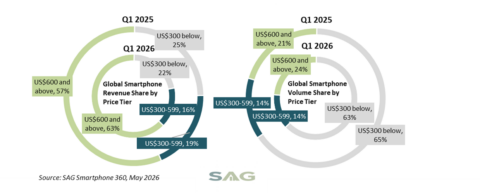

Exhibit 1: Global Smartphone Volume Share and Revenue Share by Price Tier: Q1 2025 vs. Q1 2026

Global smartphone shipments declined single digit in Q1 2026, yet total smartphone trade wholesale revenue and ASP (average selling price) posted double digit growth rate and registered the highest ever first quarter performance. Apple, Samsung and Xiaomi are on the top three list by revenue share in Q1 2026. While Samsung led the pack by shipment volume share.

The underlying price-tier migration became particularly clear during the quarter. SAG tracked the sub-US$300 smartphone segment seeing both annual shipment mix and revenue mix contraction, with volume share declining from 65% in Q1 2025 to 63% in Q1 2026, while revenue contribution fell more sharply from 25% to 22%. This indicates the traditional entry-level volume engine is gradually losing both market scale and economic importance as affordability weakens and vendors become more selective in low-end portfolio allocation.

By contrast, smartphones priced at US$600 and above continued to absorb a disproportionate share of industry upside. This premium band expanded its global shipment share from 21% to 24% year-over-year, while its revenue contribution surged from 57% to 63% during the same period. In other words, nearly two-thirds of all smartphone wholesale revenue generated globally in Q1 2026 came from devices priced above US$600, underscoring how decisively the industry’s monetization center has moved upward.

Interestingly, the US$300–599 segment did not emerge as a stronger balancing layer. While its shipment share remained broadly stable at around 14% annually, the band still lost revenue share during the quarter, indicating soft ASP expansion and limited monetization momentum in this band. This suggests the smartphone market is no longer simply broadening toward the middle; instead, value creation is increasingly skipping over the mid-band and concentrating further at the premium end where vendors retain stronger pricing power.

For smartphone vendors, Q1 2026 also highlights an increasingly important reality and shift: upstream portfolio migration is accelerating. More OEMs are now prioritizing premium and upper-mid offerings where pricing power, margin resilience, and bill-of-material cost absorption remain structurally stronger. In an environment where component inflation, geopolitical uncertainty, and slower replacement demand continue to pressure shipment growth, premium-led monetization is becoming the clearest path to defend industry value.

SAG therefore believes Q1 2026 will represent the beginning of a more durable premium-led smartphone market structure extending through 2026 and into 2027. The global smartphone industry is shifting from previous polarization towards the one-way premiumization cycle.

Clients please click here to access the full report, covering detailed smartphone shipments, trade wholesale ASP and revenue by price tier by quarter numbers through Q1 2026.