The AI smart glasses market is entering a critical inflection point. After years of early experimentation, the category is now transitioning into a high-growth phase, driven by improving use cases, ecosystem expansion, and increasing vendor participation.

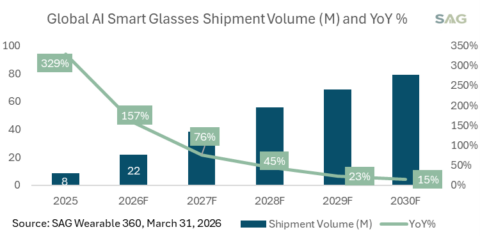

At Smart Analytics Global (SAG), we forecast global AI smart glasses shipments to reach nearly 22 million units in 2026, growing 157% YoY, with the market expected to sustain 70%+ annual growth in 2027. This rapid expansion will reshape the competitive landscape and open a new frontier in consumer devices.

Exhibit 1: Global AI Smart Glasses Volume and YoY % Forecast

Recent insights from Mark Gurman on Bloomberg provide valuable signals into how Apple is approaching this opportunity. From SAG’s perspective, Apple is focusing on the right fundamentals, but execution will ultimately determine its success.

Audio AI Smart Glasses Will Define the First Wave

The near-term market will be dominated by audio AI smart glasses with integrated camera and video capabilities, which are expected to account for nearly 90% of total shipments over the next two years.

This segment benefits from lower hardware complexity, more intuitive user interaction, and clearer everyday use cases such as hands-free capture, real-time assistance, and contextual AI services. As a result, it represents the most scalable entry point for vendors.

Apple’s expected focus on this segment aligns well with market realities. However, battery performance remains the key gating factor. Without reliable all-day usage, even the most advanced features will struggle to drive mainstream adoption.

Design, Materials, and Form Factor Are Core Differentiators

Unlike smartphones or traditional wearables, AI smart glasses are not purely technology products. They sit at the intersection of technology, fashion, and health.

This makes materials, color options, and form factor diversity critical to long-term adoption. Current offerings are largely dominated by plastic frames with limited design variation. Moving into premium materials and broader style portfolios will be essential to appeal to different consumer segments and usage scenarios.

Apple’s reported focus on exploring new materials and expanding design options is therefore a meaningful strategic move. In this category, aesthetic appeal and comfort are as important as technical capability, particularly as consumers integrate these devices into daily life.

Distribution Will Be the Deciding Factor

While product strategy is foundational, distribution and user experience will ultimately define market scale.

AI smart glasses require a fundamentally different go-to-market approach compared to smartphones or earbuds. Demo, fitting, personalization, and after-sales support are critical components of the user journey—elements that cannot be fully addressed through traditional consumer electronics channels.

Today, most vendors rely heavily on direct retail, e-commerce, and operator channels. However, scaling this category will require deeper integration with optical retailers, eyewear brands, and eyecare providers, where consumers are already accustomed to trying on, customizing, and purchasing vision-related products.

Apple brings strong advantages in brand trust and retail execution. However, expanding beyond its existing Apple Store and electronics distribution model into optical and healthcare ecosystems will be essential. Without this shift, even strong product offerings may face adoption bottlenecks.

Competitive Landscape: Apple Will Catch Up, but Meta Will Remain the Leader

Meta is expected to maintain its leadership position in the near term, with 74% global share in 2026, supported by its early mover advantage, strong product-market fit, and expanding distribution partnerships across both technology and optical channels.

However, the competitive landscape is entering a new phase as major ecosystem players begin to scale their presence. Samsung and Google are expected to enter the market in 2026, followed by Apple in 2027.

Among these new entrants, Apple is particularly well positioned to close the gap. Leveraging its integrated hardware-software ecosystem, brand strength, and global retail footprint, SAG expects Apple to scale rapidly post-entry.

We forecast Apple to become the second-largest global AI smart glasses vendor by 2028, reaching approximately 18% market share.

That said, while Apple will narrow the gap, Meta is expected to retain its leadership position over the forecast period, supported by its head start, continued iteration on core products, and strong alignment with the leading audio AI smart glasses segment.

Exhibit 2: Global AI Smart Glasses Vendor Market Share Forecast: 2o26F-2028F

Conclusion: Apple Will Close the Gap, but Leadership Will Depend on Execution

AI smart glasses are emerging as one of the most dynamic new categories in consumer technology, blending technology, fashion, and health into a single product experience.

Apple is entering the market with a strategy that focuses on the right fundamentals—prioritizing the largest product segment, investing in design and materials, and leveraging its ecosystem strengths. These factors position Apple well to scale quickly and close the gap with early leaders.

However, Meta is expected to maintain its leadership position over the near to mid-term, supported by its first-mover advantage, strong product-market fit, and expanding distribution footprint.

The next phase of competition will not be defined by hardware alone. Instead, success will depend on how effectively vendors execute across distribution, user experience, and cross-industry partnerships, particularly in integrating with optical retail and healthcare ecosystems.

Clients please click here to access the SAG AI smart glasses forecast report, covering vendor share, value share, by region and country, as well as by tech and form factors.