Following SAG’s broader overview of the global AI smart glasses market shared yesterday, this piece takes a deeper look at regional dynamics, highlighting how adoption curves will diverge across key markets.

SAG expect the global AI smart glasses market to develop unevenly across regions, with adoption shaped by ecosystem readiness, regulation, affordability, and retail infrastructure. While demand is emerging globally, the pace and form of adoption will differ significantly.

North America: The Core Growth Engine

North America will lead the market throughout the forecast period. SAG estimates that the region will account for 71% of global volume and 73% of value in 2026, supported by a well-established ecosystem, strong consumer awareness, and a highly consolidated distribution network. This includes not only traditional electronics retailers, but also optical chains, operators, and prescription eyecare providers, which are critical for enabling in-store experience and personalization.

Although North America’s share will gradually decline as other regions scale, it is still expected to remain the largest market by 2030, with 47% of global volume and 58% of value.

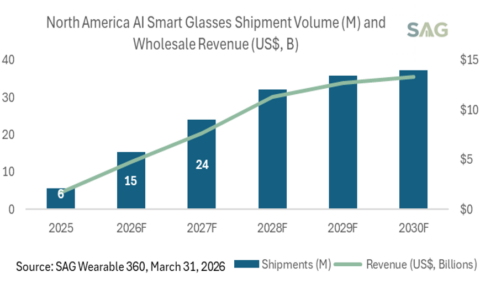

Exhibit 1: North America AI Smart Glasses Volume and Revenue Forecast

From a market size perspective, SAG forecasts North America AI smart glasses shipments to reach 15 million units in 2026 and 24 million units in 2027, generating approximately US$5 billion and US$8 billion in revenue, respectively. Early adopters in the region are primarily 25–35-year-old AR and tech enthusiasts, who are more willing to experiment with new form factors and AI-driven experiences.

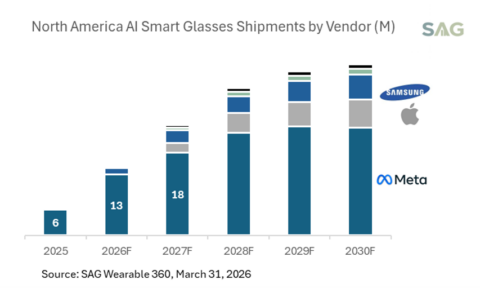

Within North America, Meta Platforms is expected to maintain its leadership position, benefiting from first-mover advantage and strong partnerships across both technology and distribution.

Apple Inc. is likely to enter the market and quickly rise into the top two vendors by 2028, leveraging its ecosystem strength and installed base. Meanwhile, Samsung Electronics is expected to remain in the third position, supported by its hardware capabilities and existing device ecosystem.

Exhibit 2: North America AI Smart Glasses Shipments by Vendor (M)

China: A Distinct and Self-Contained Ecosystem

China is expected to develop a largely distinct and self-contained AI smart glasses ecosystem, separate from the rest of the world. Due to geopolitical factors and ecosystem differences, global players such as Meta are unlikely to formally enter the Chinese market during the forecast period.

Instead, local vendors will drive adoption, similar to the divergence already seen in the smartphone industry. By 2030, SAG expects Chinese brands such as Xiaomi and Huawei to lead in volume, leveraging strong domestic distribution, competitive pricing, and deep integration with local ecosystems. At the same time, Apple is expected to lead in value, driven by its premium positioning and strong brand appeal among high-end consumers.

However, unlike North America, China’s AI smart glasses market is more heavily driven by online channels, which creates disadvantages for more complex devices such as HUD smart glasses. The lack of widespread in-store personalization, fitting, and user education can lead to higher return rates and weaker user experience. This is a key challenge that all players will need to address to unlock the next phase of growth.

Europe and Japan: Slower, More Cautious Adoption

Europe and Japan are expected to see slower adoption of HUD smart glasses, but for different reasons.

In Europe and the UK, strict privacy regulations, particularly under GDPR, create additional compliance requirements around data collection, processing, and transparency, especially for devices with cameras and real-time AI capabilities. As a result, products will launch with restricted features and a slower adoption curve.

Japan, while less restrictive from a regulatory standpoint, faces stronger social sensitivity around privacy and public recording. This behavioral factor will also limit the pace of adoption, particularly for camera-enabled and HUD devices.

Emerging Markets: Affordability and Distribution Constraints

Emerging markets, including India and Latin America, will primarily be constrained by affordability. Based on UX Connect user research, the US$400–600 range represents the pricing sweet spot for devices such as Meta Ray-Ban Display, while a US$799 price point remains too high for mainstream adoption.

In these markets, audio-based smart glasses are expected to dominate, as they provide a more accessible entry point for consumers.

Another key barrier is distribution. Online channels play a much larger role in device sales, but the lack of in-store personalization and fitting experience creates friction for users. This often leads to double-digit higher return rates, slowing category expansion and limiting user satisfaction.

Middle East and Southeast Asia: Faster Emerging Growth

Within emerging markets, the Middle East and Southeast Asia are expected to show relatively faster growth by 2030. These regions benefit from younger demographics, higher openness to new technology, and more flexible regulatory environments, making them attractive expansion markets once supply and pricing conditions improve.

From a vendor perspective, Meta, Apple, and Samsung will benefit from their global scale, strong brand recognition, and established distribution capabilities, particularly in premium segments.

At the same time, these regions are likely to become a key battleground for Chinese and second-tier players, who are more aggressive on pricing and faster in local market adaptation. Vendors such as Xiaomi Corporation and Huawei Technologies, along with other emerging brands, are well positioned to capture volume share, especially in the mid- to lower-tier segments.

In contrast, Google is unlikely to penetrate these regions quickly. SAG expects Google to prioritize North America and Europe, where its ecosystem integration, software strengths, and premium positioning are better aligned with market conditions.

Overall, the Middle East and Southeast Asia will see a more diverse and competitive vendor landscape, combining global leaders with strong regional challengers.

SAG Key Takeaway

Overall, SAG expects audio smart glasses to lead global adoption through 2030, driven by affordability and ease of use, while HUD smart glasses will scale more gradually, with adoption highly dependent on regional conditions.

The key takeaway is clear: AI smart glasses will not follow a single global adoption curve. North America will lead, China will operate independently, Europe and Japan will move more cautiously, and emerging markets will scale based on affordability and distribution readiness.

Clients please click here to access the full forecast report, which tracks and forecasts global AI smart glasses shipments, trade wholesale ASP, and revenue by major vendors across two categories—audio and HUD—covering 14 regions and countries from 2024 through 2030. It provides comprehensive analysis and insights, along with a flat file and pivot table to support in-depth and flexible analysis.