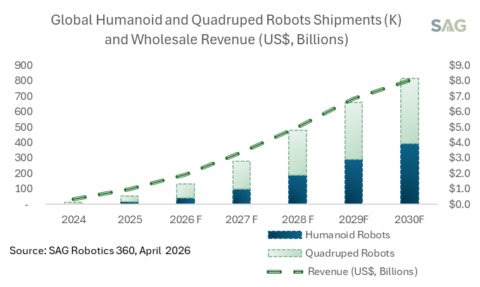

SAG estimates that global humanoid and quadruped robot shipments reached nearly 53,000 units in 2025, growing 250% year over year. Humanoid robots represented 31% of total shipments, while quadruped robots made up the remaining 69%. Trade wholesale revenue rose to US$1 billion, nearly double the 2024 level. By 2030, SAG expects the market to sustain a double-digit CAGR, with global shipments reaching 810,000 units and trade wholesale revenue climbing to US$8 billion. Even so, despite the strong momentum, several structural challenges remain beneath the surface.

Growth is Supply-Side Driven, but Demand Tells a More Cautious Story

The strong five-year growth trajectory in our forecasts is driven primarily by supply-side forces. Vendors have expanded aggressively, supported by supply chain maturation and advances in Physical AI that are improving product capability and commercial readiness. Capital and policy support have further encouraged capacity expansion. Although near-term shipments remain constrained by production capacity, the larger question is whether demand can absorb the capacity now being built.

On the demand side, we remain cautious. Our analysis across the Exploration and Validation, Industrial and Enterprise, and Consumer segments tells a different story. The Exploration and Validation segment is currently the primary growth engine, but it is likely approaching a growth ceiling, given its limited addressable scale and low repeat purchase rates. The Consumer segment remains distant for the foreseeable future, as substantial barriers persist in both categories, including price, autonomy, privacy, and home-environment design challenges.

The Industrial and Enterprise segment, in our view, has the strongest demand-side fundamentals. Enterprise customers have clear operational pain points that robots can address, larger budgets, and a clearer path to ROI. In quadrupeds, deployments in oil and gas, power grid monitoring, and data centers have already validated this. In humanoids, enterprise applications are still at an early stage, but the potential is greater than in either of the other two segments. Enterprise adoption is also a key assumption in our growth forecasts and in the industry’s healthy development. If it gains tractionand proves, the trajectory we project is achievable. If it falls short, growth will likely come in below expectations, and vendors will face rising capacity and inventory pressure.

Exhibit 1: Global Humanoid and Quadruped Robot Shipment (K) and Wholesale Revenue (US$, Billions), 2024-2030F

Quadrupeds are Commercially Proven, but Humanoids Capture the Capital

Policy, capital, and public attention do not treat humanoid and quadruped robots equally. Humanoid robotics draws significantly more enthusiasm from investors and policymakers, because the addressable market is potentially larger, the narrative resonates more, and the earlier-stage positioning offers more perceived upside.

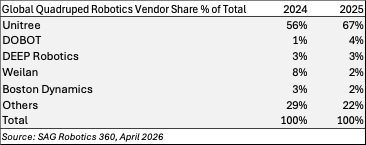

Commercial reality, however, favors quadrupeds today. SAG estimates the global quadruped market reached $350+million in revenue in 2025. Unitree held 67% of global shipments and has been profitable in its quadruped business since 2020. Boston Dynamics, though much smaller in volume, has built mature Spot deployments in oil and gas and data center environments, along with an enterprise software ecosystem and service infrastructure that remain difficult to replicate.

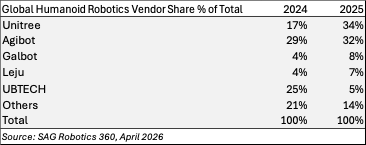

Humanoid robots tell a different story. SAG estimates the global humanoid market reached $620+ million in revenue in 2025, already exceeding quadrupeds despite fewer units shipped, reflecting higher ASPs. The market is led by Unitree at 34% of global shipments, followed closely by Agibot at 32% and Galbot at 8%. Among Western vendors, Agility has the deepest enterprise validation, while Boston Dynamics plans to begin Atlas shipments in 2026. The long-term opportunity is larger, but profitability in industrial applications remains unproven.

Exhibit 2: Humanoid Robot Vendor Shipment and Market Share in 2024 and 2025

Exhibit 3: Quadruped Robot Vendor Shipment and Market Share in 2024 and 2025

Technology is Shared, but Humanoid is Taking Center Stage

Despite the gap in commercial maturity and capital-market enthusiasm, the two categories are closely connected at the technology level. Actuators, perception systems, and AI platforms developed for one form factor can serve the other, and many vendors operate across both.

Within companies that span both markets, strategic priorities are quietly shifting toward humanoid. Unitree is a clear example. Although quadruped remains the company’s cash cow, its business mix has tilted toward humanoid in recent years, reflecting the capital and policy dynamics noted above, as well as humanoid’s higher ASPs and larger addressable market. Other vendors show a similar pattern. Xiaomi has shelved its CyberDog quadruped series to focus on humanoid development. DEEP Robotics is splitting engineering resources between quadruped and humanoid lines. Boston Dynamics, long defined by its Spot quadruped platform, is channeling significant effort into Atlas humanoid production. Whether this industry-wide shift slows quadruped product iteration is an open question worth watching.

The Market is Global, but Regional Positions are Diverging

Beyond product categories, the robotics industry is shaped by distinct regional dynamics, with each major market settling into a clearer role in the value chain. China dominates manufacturing scale and shipment volume, with Chinese vendors accounting for over 80% of quadruped and 98% of humanoid shipments in 2025. The U.S. defines the foundational technology standards and software ecosystem, from NVIDIA’s compute platform to the CUDA and Isaac ROS toolchains that underpin most robotics development globally. South Korea is investing in industrializing Western robotics technology, with Hyundai and LIG Nex1 acquiring controlling stakes in Boston Dynamics and Ghost Robotics. Europeholds certification advantages in high-value niches, with Swiss-based ANYbotics being the only vendor certified for explosion-proof industrial deployment.

These positions, however, are diverging rather than converging. Chinese vendors face growing security concerns in Western enterprise markets, while remaining dependent on NVIDIA’s Jetson platform for AI inference. Western vendors do not participate in China’s supply chain ecosystem, resulting in structurally higher costs and slower hardware iteration. Each side carries constraints that the other does not face. Under the current geopolitical environment, both sides are responding by seeking alternatives rather than deeper interdependence, making the emergence of two relatively independent ecosystems increasingly likely. How much technology can flow between them will depend on future policy decisions.

SAG Takeaway

SAG believes the robotics market will grow robustly through 2030, but the path depends on whether Industrial and Enterprise adoption can keep pace with supply-side expansion. Quadruped robots have a more proven commercial foundation, while humanoid robots carry the larger long-term opportunity. In both categories, the next two to three years will be decisive. Vendors that can demonstrate replicable, scaled enterprise deployments will pull ahead. Those that cannot, particularly vendors that expanded capacity ahead of validated demand, will face growing consolidation pressure from 2027 onward.

Clients, please click here to access the comprehensive reports covering humanoid and quadruped robot shipments, average wholesale ASP and revenue, and vendor market share data from 2024 through 2030.