At Mobile World Congress (MWC) 2026, robotics was not the central theme of the show floor, which remained firmly anchored in the mobile communications ecosystem. However, Smart Analytics Global (SAG) observed a noticeable uptick in robotics presence—particularly from Chinese vendors—adding fresh energy and cross-industry momentum to the event. While still early in the commercialization cycle, the latest demonstrations underscore that robotics is gradually converging with connectivity, AI, and edge computing, areas closely tied to the mobile industry’s long-term roadmap.

Growing Global Participation Beyond China

China continues to lead the humanoid robotics ecosystem in terms of vendor scale, supply chain depth, and commercialization momentum. However, MWC 2026 also highlighted a gradually broadening global field. SAG observed participation from South Korea and Vietnam, signaling that robotics innovation is becoming more geographically diversified.

A notable presence came from LIG Nex1, a South Korean defense technology company founded in 1976, which is actively expanding into robotics, AI, and unmanned military systems. The company recently strengthened its position through the acquisition of a 60% stake in Ghost Robotics, a developer of quadrupedal robots. At MWC, LIG Nex1 demonstrated its robot dog capabilities alongside broader unmanned platforms including the G-Sword combat robot, unmanned surface vehicles (USVs), and the LEXO wearable muscle-assistance system. These demonstrations added meaningful depth to the robotics presence on the show floor.

SAG also noted early-stage humanoid robot showcases from Vietnamese manufacturers. While still nascent compared with Chinese leaders, their participation reinforces the view that the humanoid robotics race is expanding beyond a single-country narrative.

Humanoid Robots: Progress Visible, but Home Adoption Will Take Time

SAG estimates that global humanoid robot sales exceeded 13,000 units in 2025, led primarily by Agibot and Unitree, which together accounted for roughly 66% market share. Despite growing media attention and rapid technical iteration, the humanoid robot segment remains in an early commercialization phase.

Current deployments are still concentrated in demonstration and promotional performances, R&D and academic platforms, and limited productivity or pilot deployments. From SAG’s perspective, the key bottleneck remains the gap between technical capability and reliable, cost-effective home service deployment. While vendors continue to showcase improvements in mobility and interaction, real household adoption will require meaningful advances in safety validation, task reliability, battery endurance, and significant cost reduction.

As a result, SAG expects industrial and commercial environments to remain the primary landing zone for humanoid robots over the next several years. Logistics support, guided reception, education, and controlled enterprise settings provide more structured environments where current technology can deliver clearer return on investment.

Government Funding Fuels Early-Stage Expansion

One of the most important structural drivers behind the rapid emergence of the humanoid ecosystem in China has been strong government support. Public funding, local industrial policies, and innovation incentives have helped accelerate R&D activity, startup formation, and early pilot deployments.

This policy tailwind is contributing to what SAG describes as a “mushrooming phase” of the humanoid robotics industry. However, the transition from policy-supported growth to sustainable commercial demand will be the critical milestone to watch through the late 2020s.

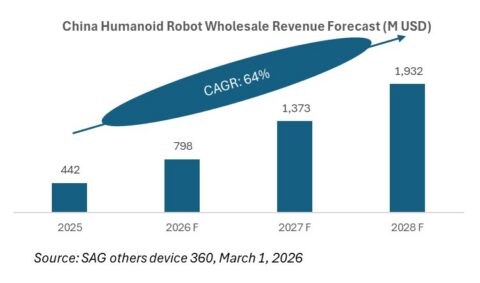

SAG forecasts the China humanoid robot market will maintain double-digit annual growth, reaching approximately $1.9 billion by 2028, though the path will likely remain uneven and heavily enterprise-led in the near term.

Robot Dogs: Faster Commercial Curve Emerging

In contrast, quadruped robot dogs are demonstrating a meaningfully faster commercialization trajectory. Compared with humanoid robots, robot dogs benefit from lower mechanical complexity, more clearly defined vertical use cases, earlier enterprise adoption, and a more favorable near-term cost structure.

SAG observes that robot dogs already support a broader range of practical applications, including industrial inspection, security patrol, energy site monitoring, and specialized public safety scenarios. These deployments provide clearer short-term ROI, which is accelerating procurement decisions among enterprise and government buyers.

As a result, the robot dog segment has already surpassed humanoid robots in commercial maturity and is expected to maintain a steeper growth curve over the next several years.

Why Robotics Matters at a Mobile-Centric Event

Although MWC remains fundamentally a connectivity and mobile ecosystem event, the presence of robotics vendors is strategically meaningful. Robots are becoming increasingly dependent on 5G and 5G-Advanced connectivity, edge AI processing, sensor fusion, and real-time data transmission—capabilities that sit squarely within the mobile industry’s innovation stack.

This convergence suggests robotics will gradually become a natural extension of the broader intelligent device ecosystem that smartphone vendors, operators, and AI platform players are building toward.

SAG Conclusion

MWC 2026 confirms that humanoid robots are advancing technically but remain several years away from meaningful household penetration. Enterprise and industrial deployments will continue to dominate the near-term opportunity, supported in part by government investment.

Meanwhile, robot dogs are moving along a faster commercialization path, benefiting from clearer use cases and lower system complexity, as well as the lower cost. The growing participation from South Korea and Vietnam further indicates that the competitive landscape is broadening globally, even as China maintains a clear leadership position. For the broader intelligent device ecosystem, robotics is no longer peripheral. It is emerging as an important long-term growth vector closely tied to connectivity, AI, and edge computing evolution.