Key Takeaways

• The NVIDIA-LG partnership highlights a growing trend of robotics supply chain diversification amid rising U.S.-China geopolitical tensions.

• While China leads humanoid robotics in scale and cost, leading Chinese vendors remain highly dependent on NVIDIA’s AI computing platforms.

• Export controls on advanced chips and critical rare earth materials are creating new structural risks for the global robotics industry.

• LG brings NVIDIA beyond industrial robotics into consumer and home robotics, leveraging its leadership in home appliances and smart home ecosystems.

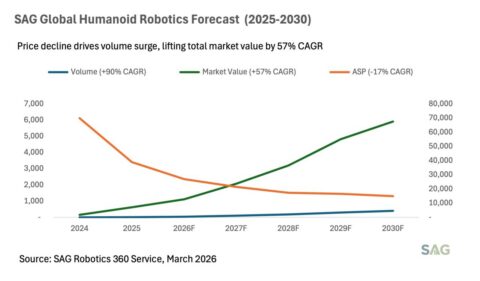

• SAG forecasts global humanoid robot shipments will grow at a CAGR of over 90% during the next five years, though mass-market adoption remains 5-10 years away.

This week, NVIDIA and LG Electronics announced an expanded partnership focused on AI, robotics, digital twins, and next-generation automation. While the announcement centers on technology collaboration, SAG believes it reflects a broader trend that deserves greater attention: the growing geopolitical risks surrounding the global humanoid robotics industry.

China currently leads the humanoid robotics market in terms of volume, manufacturing scale, and cost competitiveness. Chinese vendors have successfully accelerated commercialization by leveraging a mature supply chain, strong government support, and aggressive investment. However, SAG observes that rising geopolitical tensions are increasingly casting a shadow over the industry’s long-term development.

The U.S.-China competition in humanoid robotics is unfolding along multiple dimensions.

On semiconductor technology, Chinese humanoid robot vendors remain heavily dependent on NVIDIA platforms. Many leading Chinese robotics companies continue to utilize NVIDIA GPUs and AI computing solutions for training, simulation, and deployment. While domestic Chinese semiconductor alternatives are improving, they still lag behind NVIDIA in both performance and ecosystem maturity.

At the same time, China has imposed export controls on several critical rare earth elements, creating new uncertainties for the supply of permanent magnets used in electric motors and robotic actuators. These materials remain essential building blocks for humanoid robots.

Meanwhile, policy risks are increasing in the United States. Congressional actions and legislative proposals have increasingly targeted Chinese robotics companies, citing national security concerns and calling for tighter export controls, procurement restrictions, and market access limitations. As humanoid robots become increasingly capable and connected, regulatory scrutiny is likely to intensify.

NVIDIA’s growing collaboration with LG can be viewed through a broader strategic lens. Diversifying beyond Chinese robotics customers allows NVIDIA to reduce geopolitical exposure while expanding its ecosystem across South Korea, North America, Europe, and other markets.

The partnership extends beyond industrial automation. LG plans to deploy NVIDIA’s digital twin and simulation platform, Isaac Sim, across its global manufacturing operations to accelerate factory optimization and robotics development.

More importantly, LG brings a unique advantage to the humanoid robotics race. While many competitors focus primarily on industrial and warehouse applications, LG is a global leader in home appliances and consumer electronics. The company is integrating NVIDIA’s GR00T foundation model and robotics technologies into modular robots and future home robotics platforms. This could help extend humanoid capabilities beyond factories and warehouses into household assistance, smart home management, and everyday domestic tasks.

For NVIDIA, robotics remains a relatively small portion of its business today, but its importance is growing rapidly. NVIDIA’s Automotive and Robotics division generated a record US$2.3 billion in revenue during the most recent fiscal year, up 39% year-over-year. While automotive remains the dominant contributor, SAG expects robotics to account for an increasingly meaningful share of revenue over the coming years as commercialization accelerates.

SAG forecasts global humanoid robot shipments will grow at a CAGR exceeding 90% over the next five years. However, widespread adoption remains a longer-term story. Significant improvements are still required in cost, reliability, safety, reasoning capability, and regulatory frameworks before humanoid robots can achieve mass-market deployment.

Exhibit 1: SAG Humanoid Robot Volume and Value Forecast

The humanoid robotics race is no longer solely about technology leadership or manufacturing scale. Increasingly, it is also about supply chain resilience, ecosystem control, and geopolitical risk management. The NVIDIA-LG partnership is another signal that the industry is beginning to adapt to this new reality.