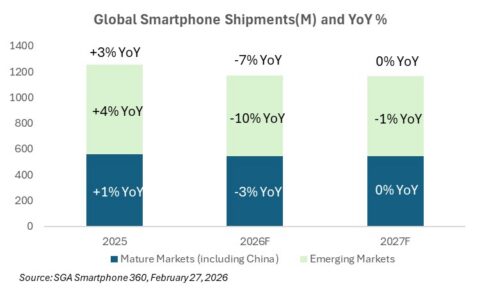

Smart Analytics Global (SAG) forecasts global smartphone shipments will decline 7% year over year to 1.17 billion units in 2026, primarily driven by elevated component costs and resulting device price increases.

The downturn is expected to be stronger in emerging markets, where low-cost smartphones represent a larger share of total volumes and consumer price sensitivity remains high. SAG projects double-digit declines across several emerging regions, while mature markets, including North America, Western Europe, Japan, South Korea, Greater China, and selected developed Asian economies, are likely to see a more modest adjustment of around 3% year over year in 2026.

Within the emerging world, Central Latin America, Africa, and Southwest Asia (including India) are expected to experience the steepest declines, while the Middle East and Southeast Asia should perform relatively better with high single-digit contractions.

Looking ahead to 2027, SAG expects the global smartphone market to remain broadly flat year over year. Mature markets are likely to stabilize along a similar trajectory, while emerging markets may continue to face downward pressure, though the pace of decline should narrow meaningfully as pricing dynamics and supply constrain will be gradually normalized, starting from the second half of 2027.

From a vendor perspective, SAG expects Apple and Samsung to gain incremental market share, largely at the expense of Chinese OEMs including Xiaomi, Transsion, and BBK Group brands, as well as numerous smaller vendors that maintain heavier exposure to the entry-level segment. Among Chinese vendors, Huawei appears better positioned due to its stronger premium mix, higher domestic China exposure, and increasing reliance on self-sufficient component sourcing, while Honor is also expected to outperform most peers as its overseas portfolio continues shifting toward mid- and high-tier segments.

SAG has observed that smartphone vendors have begun implementing price increases across most price bands in recent months, with the trend accelerating from February and additional adjustments likely through March. Importantly, the magnitude of these increases remains relatively contained, generally below 10% across most models, indicating vendors are carefully managing pricing to avoid significant consumer pushback. In mature markets, the impact should remain manageable given the widespread use of installment plans and carrier subsidies, whereas in emerging markets the higher price elasticity, particularly in the low-end segment, is likely to translate into more meaningful demand pressure.

As Chinese vendors retreat in the low tiers, SAG believes Samsung is best positioned to capture the resulting volume gap in the low-end segment, provided the company can secure sufficient in-house chipset supply. Samsung’s relatively higher margin structure compared with most Chinese competitors also provides greater flexibility to balance pricing and volume. Apple is similarly well positioned; while the upcoming iPhone 18 series is unlikely to replicate the super-cycle dynamics of the iPhone 17 generation, Apple can leverage its legacy iPhone portfolio and the recently introduced iPhone 17e to push further into mid-tier price bands and capture incremental share from Android competitors.

Despite unit softness, SAG expects global smartphone wholesale ASP to post high single-digit growth in 2026, broadly stabilizing total market revenue. In 2027, supported by a richer premium mix, including the potential contribution from higher-priced foldable iPhones, ASP growth should accelerate further, allowing global smartphone wholesale revenue to return to a modest growth trajectory even as overall shipment volumes remain flat.