The ongoing conflict involving Iran is creating new risks for the global smartphone industry at a time when the market is already facing rising component costs and weakening consumer demand.

The escalation has disrupted energy markets, pushed oil prices sharply higher, and raised concerns about trade routes and industrial supply chains. The Middle East conflict has already removed significant oil supply from global markets and driven crude prices above $100 per barrel in recent weeks.

From Smart Analytics Global’s perspective, the conflict could impact the smartphone industry through two major channels: supply-side disruption and demand-side weakness.

Supply-side risks could push smartphone costs higher

One immediate impact comes from rising energy prices, which directly affect semiconductor and electronics manufacturing. Chip fabrication plants and electronics assembly lines are highly energy-intensive, meaning sustained oil and gas price increases can raise manufacturing costs across the technology supply chain.

Another risk involves raw materials and industrial gases used in semiconductor production. The Middle East plays a role in supplying several feedstocks and materials used in the semiconductor ecosystem, including petrochemical derivatives such as naphtha, methanol and ammonia, as well as industrial gases like helium. Helium is particularly critical for semiconductor fabrication and cooling processes, and countries such as Qatar are among the world’s major suppliers.

Industry concerns have already emerged that disruptions in the region could tighten supply of semiconductor materials and push chip prices higher.

Logistics disruption is another key risk. Dubai functions as one of the world’s most important aviation and cargo hubs connecting Asia with the Middle East, Europe and Africa. According to Smart Analytics Global tracking, air freight remains the primary transportation channel for high-value consumer electronics such as smartphones, rather than sea freight.

Although Dubai has worked to restore flight operations as much as possible, transportation disruptions and higher fuel costs could significantly raise air cargo rates. Higher logistics costs would ultimately push smartphone prices higher globally, further aggravating the impact of existing memory and component shortages.

Demand could weaken further under geopolitical uncertainty

Beyond supply disruptions, the conflict could also weaken global smartphone demand, particularly in emerging markets.

Rising inflation, higher fuel costs and geopolitical uncertainty typically reduce consumer confidence and discretionary spending. Smartphones have already experienced noticeable price increases in recent months as manufacturers pass through higher component costs, particularly memory.

The demand impact could be more severe in emerging markets, including parts of Southeast Asia and smaller economies that rely heavily on imported energy and have limited strategic reserves. In these markets, higher oil prices quickly translate into broader inflation pressure, reducing consumers’ purchasing power for discretionary products such as smartphones.

Some governments have also begun encouraging energy-saving measures, including promoting work-from-home policies or reduced commuting in order to limit energy consumption. Similar measures were widely implemented during the COVID period. While these policies may help stabilize energy demand, they can also slow retail activity and consumer spending, further weakening smartphone upgrade cycles in price-sensitive markets.

As a result, emerging markets—which historically account for a large share of global smartphone shipment volumes—could see a sharper slowdown in device demand if geopolitical tensions persist.

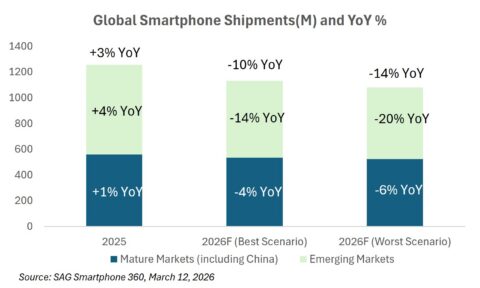

SAG scenario outlook for the global smartphone market

Smart Analytics Global previously forecast global smartphone shipments to decline 7% year over year in 2026, reflecting rising component costs and softer consumer demand.

Given the potential impact of the ongoing conflict, SAG now outlines two possible scenarios for the smartphone market.

Scenario 1 – Conflict ends within one month (by end-March)

If the conflict is resolved relatively quickly, disruption to supply chains and consumer sentiment would remain manageable.

Under this scenario:

Global smartphone shipments decline 10% YoY to around 1.13 billion units in 2026

Mature markets (including China) decline 4% YoY in 2026

Emerging markets decline 14% YoY in 2026

Scenario 2 – Conflict lasts three months (through end-June)

A prolonged conflict would intensify energy price pressure, logistics disruptions and consumer demand weakness.

Under this scenario:

Global smartphone shipments decline 14% YoY to around 1.08 billion units in 2026

Mature markets decline 6% YoY in 2026

Emerging markets decline 20% YoY in 2026

Comparing the potential impact with the COVID disruption

For context, the global smartphone market has already experienced two major downturns during the COVID period.

In 2020, when the COVID outbreak triggered lockdowns across many countries, global smartphone shipments declined 8% year over year. However, the demand impact was partially offset by increased purchases of secondary devices, as many consumers bought additional smartphones, tablets and PCs to support work-from-home and study-from-home needs.

In 2022, the market faced a much deeper decline of 12% YoY. This downturn was driven primarily by supply-side disruptions, particularly large-scale manufacturing shutdowns and logistics interruptions caused by lockdowns in China. Production constraints and supply chain bottlenecks had a greater impact on shipments than demand itself.

Smart Analytics Global (SAG) estimates that the conflict could push the 2026 global smartphone market decline to between 10% and 14% year over year, depending on how long geopolitical tensions disrupt energy markets, semiconductor supply chains and global logistics.

Higher oil prices, potential disruptions to semiconductor materials supply, and rising air freight costs could increase manufacturing and transportation expenses across the smartphone supply chain. At the same time, inflation pressure and geopolitical uncertainty may weaken consumer demand, particularly in emerging markets where purchasing power is more sensitive to energy price shocks.

Taken together, these supply and demand pressures could deepen the downturn already expected in the global smartphone market in 2026.

Conclusion: A New Macro Shock for the Smartphone Industry

The Iran conflict introduces a new layer of uncertainty for the global smartphone industry at a time when the market is already facing rising component costs and soft consumer demand.

From Smart Analytics Global’s perspective, the key risk lies in the combined pressure on both supply and demand. Higher oil prices, rising logistics costs, and potential disruptions to semiconductor materials supply could increase smartphone manufacturing costs. At the same time, inflation and economic uncertainty may weaken consumer purchasing power, particularly in emerging markets where smartphone demand is more sensitive to price increases.

Based on current developments, SAG believes the global smartphone market could decline between 10% and 14% year over year in 2026, depending on how long the conflict continues to affect energy markets and supply chains.

Under the most likely scenario, where the conflict stabilizes within a relatively short period (end of March), the market downturn would remain manageable but still deeper than previously expected. However, if geopolitical tensions persist and energy prices remain elevated for several months, the global smartphone market could face a decline even greater than the pandemic-driven downturn seen in 2022.

Smart Analytics Global will continue to monitor developments closely and update its global smartphone forecast as the geopolitical situation evolves.